The last few weeks have been tough for natural resource investors. Pretty much every single metal across the board has been performing poorly over the last few weeks and junior mining stocks have not been spared. There is one metal, however, which lately has been giving investors a glimmer of hope…

LITHIUM

Since the start of the year, Lithium has been the worst performing metal by a long shot. Looking at the chart below, the price of Lithium started the year around 500,000 CNY per tonne and bottomed out around 165,000 CNY per tonne on April 26th – a drop of over 68%. This was largely due to concerns about poor demand levels for EV’s, particularly in China. The drop in demand coincided with a significant oversupply of batteries in the period as producers took advantage of final inflows of government subsidies and ramped up production until the end of 2022, creating unsustainably high inventory levels. However, over the last couple of weeks, the price of Lithium has started to rebound in a MAJOR way.

Since bottoming out at the end of April, the price of Lithium has rebounded to 225,000 CNY (+36%) per tonne amid renewed optimism for electric battery demand. Analysts are forecasting that Lithium demand by 2040 will be 16 times higher than present-day levels. The fact is, the long term fundamentals for Lithium are still intact and better than ever.

M&A Heating Up in the Lithium Space

With the drop in Lithium prices starting to plateau, the potential for opportunistic mergers and acquisitions within the Lithium space is very high. Valuations on high-quality developers have dropped significantly and larger Lithium producers are looking to protect their market share by buying developing assets on the doorstep of new EV supply chain build-outs.

Stifel GMP recently put out a note to clients highlighting exactly this:

“This past week, we saw China spot prices realize their first weekly gain since November, with spot battery-grade carbonate up 3% week-over-week. Valuations within the Lithium space have responded, in part. Within our coverage universe, the Lithium developers are trading at a P/NAV of 0.44x, versus a 12-month average of 0.53x and a high of 0.58x in early February. With the mining industry’s financial strength at or near 20-year highs, M&A is the preferred avenue for growth. That the metals and mining industry, and specifically Lithium industry, could be entering a new wave of merger and acquisition activity should come as no surprise.”

We have already started to see evidence of M&A activity in the Lithium space with Albemarle’s rejected $3.7 billion cash offer for Liontown Resources (ASX:LTR). Liontown controls two major Lithium deposits in Western Australia, including its flagship Kathleen Valley project. The project is one of the world’s largest and highest-grade hard rock Lithium deposits and is expected to go into production in 2024.

Another example is Tecpetrol Investments’ recent take-over offer to Alpha Lithium for CAD$241 million, which was also rejected. Alpha Lithium is currently engaged in the development of Lithium salars in Argentina.

It is evident that producers are currently on the hunt for high-quality Lithium development assets with near-term production potential — so who could be next on their list?

Lithium Chile – A High-Quality, Lithium Development Play

The smartest way to play the Lithium rebound is to pick high-quality Lithium development companies which have near-term takeover potential.

The first company that comes to mind for me is Lithium Chile (TSXV:LITH)(OTCQB:LTMCF), which is a company I have written about it in the past.

In my last article on Lithium Chile, I highlighted the company’s near-term takeover potential and suggested a few different scenarios of how a buyout may look. Not long after, the company ended up putting out a news release which described how the company had already received expressions of interest for the acquisition of certain properties. I strongly believe these expressions of interest were for Lithium Chile’s Arizaro project, which is actually located in Argentina, and I also strongly believe that these expressions of interest are still in play — now more than ever.

Determining the Value of a Takeover

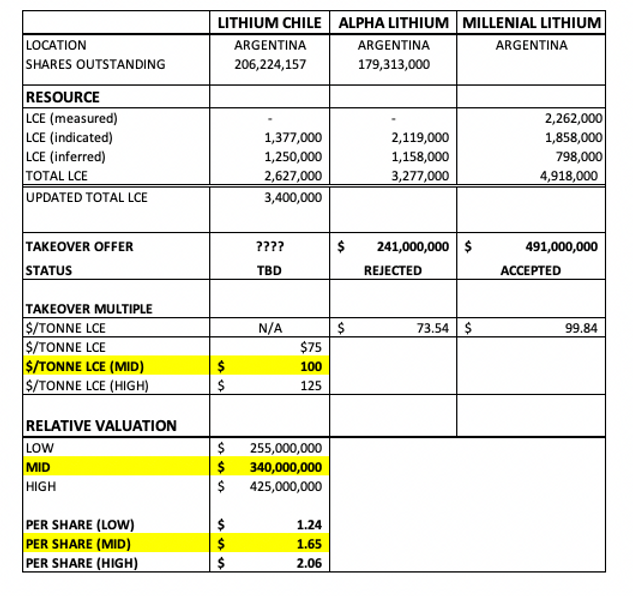

So if a takeover offer for Lithium Chile were to come through, what would the numbers look like? If we want to determine the potential takeover value of Lithium Chile’s Arizaro project then all we need to do is compare it with recent takeover bids in the space. If Tecpetrol is willing to pay $241M for Alpha Lithium, which has 3.27M tonnes of Lithium in Argentina, then the take-over value of Arizaro should be similar.

Alpha Lithium, which recently received a CAD$241 million takeover offer, has 2,119,000 tonnes LCE in the indicated category and 1,158,000 in the inferred category — so 3.27M tonnes of LCE in total. This comes out to a $73/tonne take-over multiple.

Keep in mind that this offer was rejected as Alpha Lithium did not feel it was sufficient. In reality, it was a lowball offer – Tecpretrol has already come out and said that it remains prepared to engage with Alpha immediately in good-faith negotiations and improve its offer based on due diligence. Clearly, a $73/tonne is too low. To find a more reasonable multiple, let’s look at another acquisition which took place in 2022.

Take Millennial Lithium for example…. On January 25th, 2022, Millennial Lithium was sold to Lithium Americas Corp. for CAD$491 million. At the time of the acquisition, Lithium prices were right around $250,000 CNY/T, so not much higher than they are today. Millennial Lithium had a total of 4.918M tonnes of LCE — so they were acquired at a multiple of roughly $100/tonne LCE.

I believe a minimum of $100/tonne LCE multiple is more applicable in determining the valuation of $LITH.

The last resource estimate that Lithium Chile put out on December 5th, 2022 showed 2.6M tonnes of LCE in the ground. Since then, the company has drilled multiple successful wells which, based on my calculations, should add another ~800,000 tonnes of LCE to the current resource, bringing the total current resource to 3.4M tonnes of LCE.

Using a $100/tonne multiple on Lithium Chile’s 3.4M tonne resource, the valuation of Arizaro’s resource can be pegged at $340,000,000, which comes out to around $1.65 per share. This would be a +120% gain from the current share price of $0.75.

At the moment, Lithium Chile is trading for a ~$150M market cap. With a 3.4M tonne resource, that is equivalent to around $44/tonne LCE — the company is significantly undervalued at current prices.

Remember that these numbers are ONLY factoring in the valuation of Arizaro and does not account for ANY of the +130,000 hectares of sought-after land that the company has in Chile which also holds significant value.

Do Not Let “Nationalization” Scare You Away

Now, you may be aware of recent developments in Chile regarding Lithium and their attempts to nationalize the commodity. DO NOT let this put you off of investing in Lithium Chile.

First off, despite being named Lithium “Chile”, the company’s flagship asset, Arizaro, is actually located in Argentina. While they do have a massive portfolio of exploration assets in Chile, these assets are still in the exploration stage. LITH’s development project, which has an indicated and inferred resource of 2,587,000 tonnes of Lithium equivalent (LCE), is located in Argentina.

Secondly, more recent statements from Chile’s President suggest that Chile’s plans to nationalize Lithium are not really “nationalization”, but rather a partnership between private companies and the state to create a transparent way for private companies to explore and develop their assets.

Steve Cochrane, President & CEO of Lithium Chile had this to say about it:

“The announcement from President Boric yesterday will pave the way for private companies to be able to advance their projects in Chile. Contrary to nationalizing the Lithium industry in Chile, they have established a partnership between the public and private sectors that should allow for the rapid development of Lithium projects in Chile. It is our opinion that removing the uncertainty around developing Chile’s Lithium assets will create a lot of global interest in Chilean Lithium projects and with our large exploration portfolio we are uniquely positioned to capitalize on this revolutionary decision.”

The Bottom Line

The recent rebound in Lithium prices and the potential for mergers and acquisitions in the Lithium space have brought a glimmer of hope to natural resource investors. Despite being the worst-performing metal earlier in the year, Lithium has experienced a significant recovery, driven by renewed optimism for electric battery demand and long-term growth prospects. The mining industry’s financial strength and the desire of larger producers to secure developing assets have created favourable conditions for M&A activity. This trend is exemplified by Albemarle’s rejected cash offer for Liontown Resources and Tecpetrol Investments’ unsuccessful bid for Alpha Lithium. Considering the potential takeover value of Lithium Chile’s Arizaro project, similar to recent acquisitions, suggests a valuation of $340 million or around $1.65 per share, representing a substantial gain from the current share price. Additionally, concerns about Chile’s plans to nationalize Lithium should not deter investors, as Lithium Chile’s flagship asset is located in Argentina, and recent statements indicate a partnership approach between private companies and the state.

Overall, Lithium Chile emerges as a high-quality Lithium development play with near-term takeover potential and an opportunity for investors to capitalize on the positive momentum in the Lithium market.

– SmallCapInvestor

DISCLOSURE

The author of this article has received compensation in the amount of CAD $10,000 to write the report about the company mentioned herein. The purpose of this compensation was to cover the author’s time, research, and expertise in analyzing the company. It is important to note that the payment received may create a potential conflict of interest, as the author may be influenced by the compensation received. Readers are advised to consider this disclosure when evaluating the credibility and objectivity of the information provided in the article. While the author has made reasonable efforts to ensure the accuracy and reliability of the content, readers should conduct their own research and analysis and seek independent financial advice before making any investment decisions related to the small cap company mentioned. The compensation received by the author does not guarantee or imply any specific outcome or recommendation regarding the small cap company’s investment potential. This disclosure is intended to provide transparency and assist readers in understanding the context in which the article was written.